Is buying a home always better than renting

Client profile

Alisha

30-year-old, single, with a stable full-time income

First-time home buyer purchasing for personal use

Looking for a 1–2 bedroom apartment

Prioritizes living within walking distance to work and social circle

Uncertain about staying in the city for the next 5+ years

Paths explored

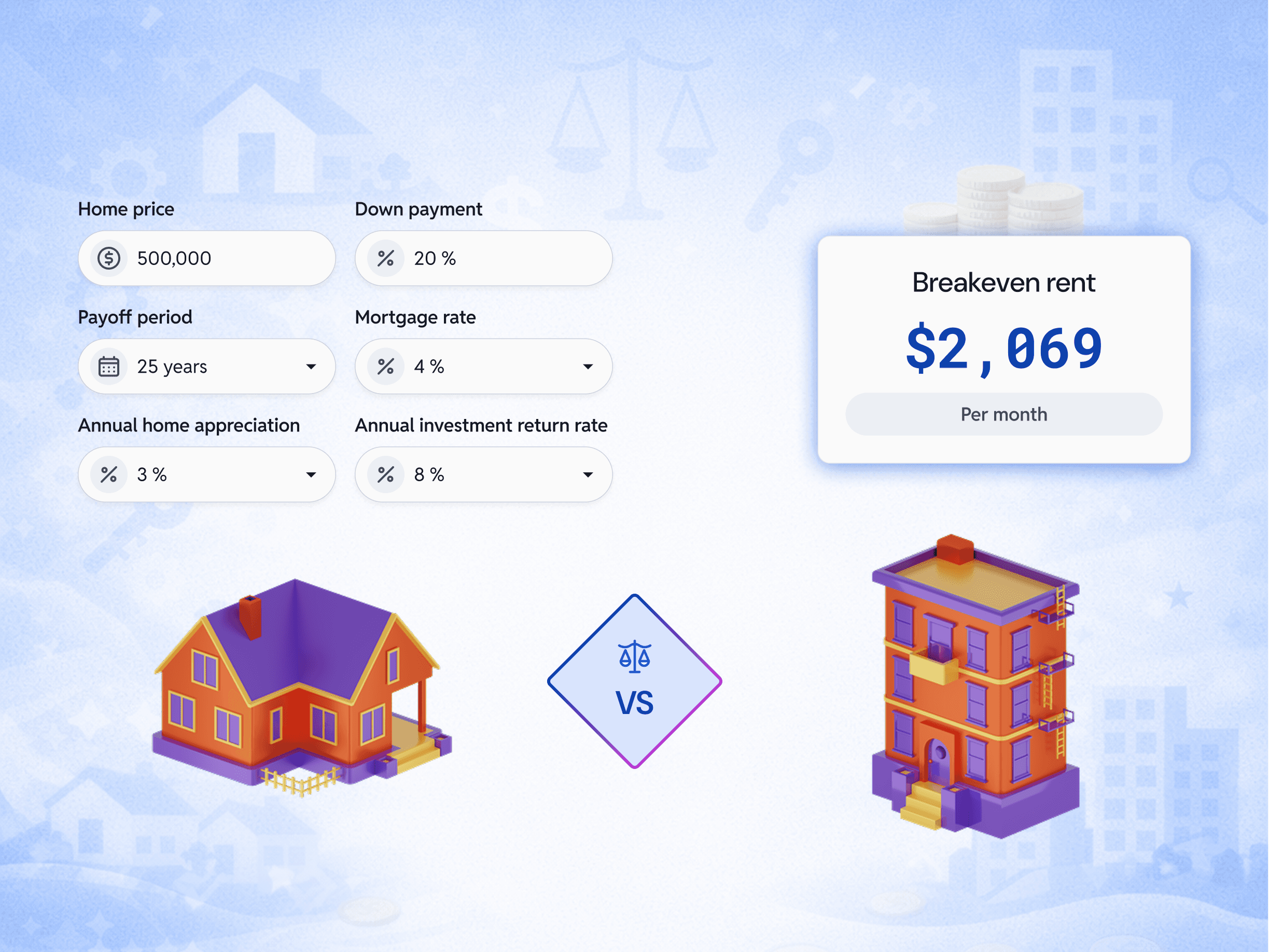

Path 1 — Buy now and hold long-term

Higher monthly cost, but builds equity over time

Works well if lifestyle and location remain stable

Conclusion:

Since the market rent (~$2,400) is above the breakeven point, buying is financially favourable in this scenario.

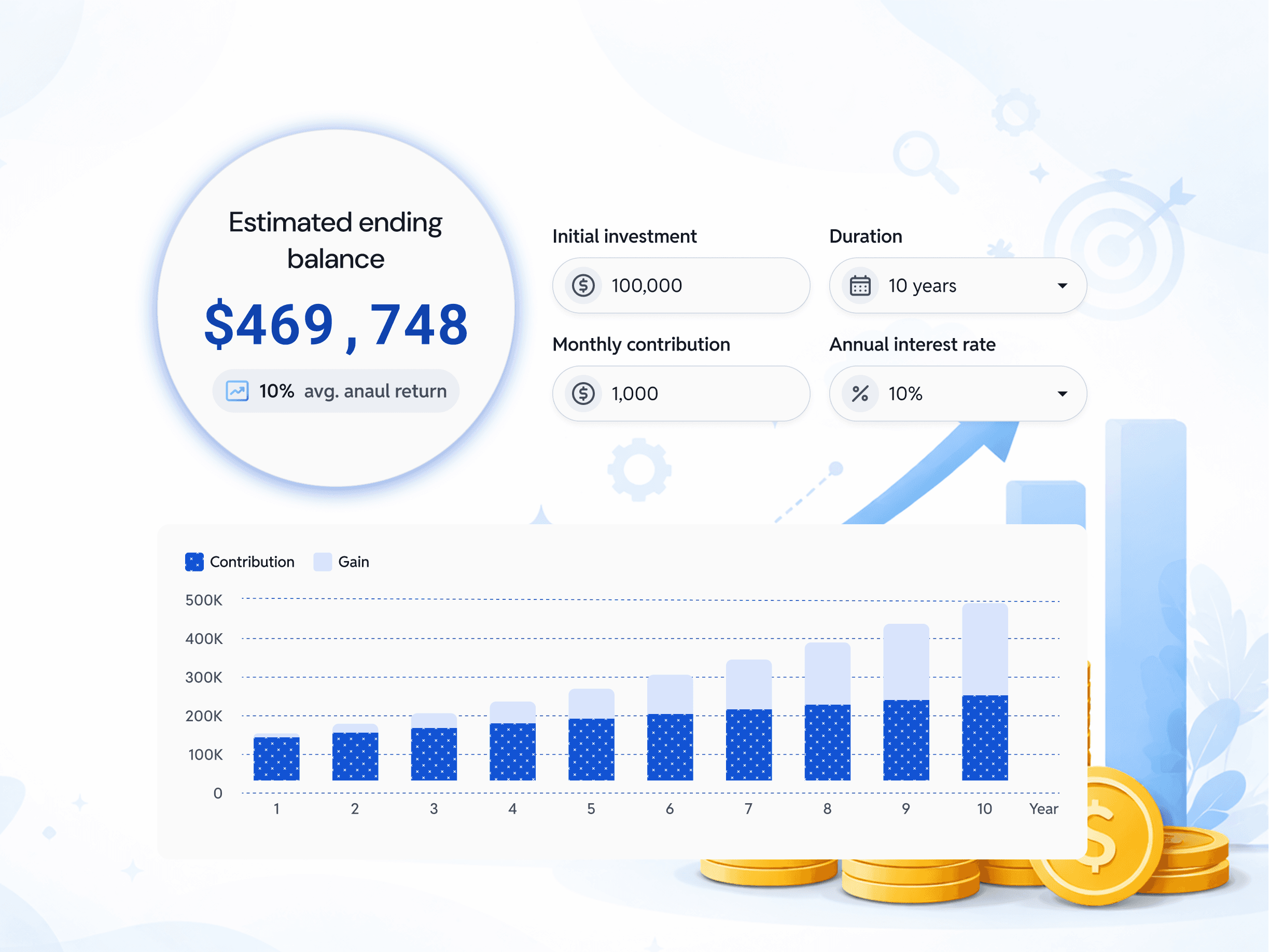

Path 2 — Rent and invest the difference

Assuming all upfront costs and monthly savings are invested

Assuming fixed rent. Rising rent can reduce how much can be invested over time, thus reducing returns.

Conclusion:

Investment returns are similar to the final home value (~$820K), but can drop if rent rises or savings are not invested consistently.

Path 3 — Buy now and sell in ~5 years

Buying gains come from leveraging a larger asset (home value vs invested cash)

Selling costs reduce buying gains, but do not fully offset the leverage benefit

Conclusion:

Buying is slightly better because it benefits from leverage on a larger asset, but the gap is small and can easily flip with changes.

Recommendation

Buy if Alisha plans to stay long-term. If the timeline is uncertain, renting and investing offer similar or slightly better returns with more flexibility.

What could change this decision?

👉 Time horizon

Planning to stay longer → Buy, because upfront and selling costs are spread over more years

Likely to move soon → Rent, because short-term ownership is more sensitive to transactional costs and market changes

👉 Rental price

Rent is too high → Buy, because renting becomes more expensive relative to owning

Rent is low → Rent, because more savings can be invested and grow over time

👉 Investment return

If it increases significantly → Rent, because invested savings grow faster

If it decreases significantly → Buy, because renting loses its compounding advantage

👉 Home appreciation

If it increases significantly → Buy, because gains from a larger asset are amplified

If it decreases significantly → Rent, because ownership gains are limited

👉 Investment discipline

Confident you will invest consistently → Rent, because consistent investing maximizes returns

Likely to spend the difference → Buy, because ownership forces saving through equity

👉 Mental security

Want stability and don’t want to move → Buy, because control and certainty matter more

Value flexibility or be uncertain about plans → Rent, because it keeps options open

Used tools

Investment growth projection calculator

# retirement

# compound-interest

Your consistent contributions and compound growth can build substantial wealth over time.

Buy vs. Rent calculator

# property

# opportunity-cost

Compare buying vs renting by factoring in opportunity cost and the full cost of ownership.

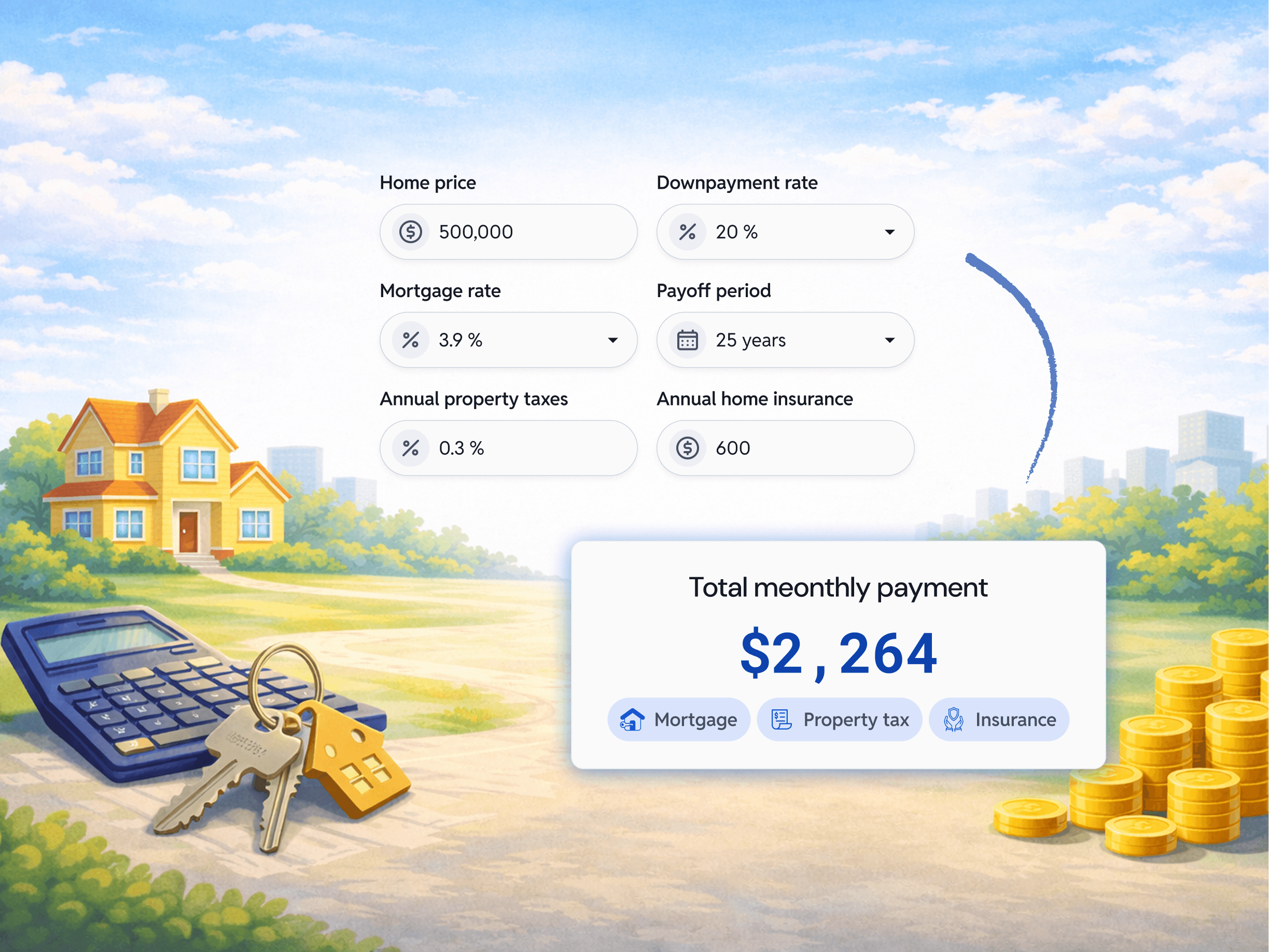

Home ownership cost breakdown

# affordability

# mortgage

# home-ownership

Calculate the monthly cost of owning a home by factoring in mortgage, taxes, and ongoing expenses.